Mortgage Bankers Association (U.S.); MCT

Mortgage Bankers Association (U.S.); MCT

World News Desk

Learn the why behind the headlines.

Subscribe to the Real Truth for FREE news and analysis.

Subscribe NowThe U.S. Commerce Department reported that construction of new homes and apartments dropped 6.1% in July 2007, down 21% from July 2006, to the slowest pace since January 1997. This cooling of the market does not appear to be a short-term trend.

In July, the number of applications—perhaps the best indicator of future construction activity—fell by almost 3% nationally. Ironically, two of the regions hit particularly hard by these declines have been symbols of recent economic growth: the American South and West, with construction slumping 11% and 3.7%, respectively.

What have been the consequences of this recent slowdown? Builders across the nation have begun to slash building prices, offering aggressive buying incentives in an effort to induce sales of recently built homes and to stimulate the “pre-sale” of new homes.

Despite these efforts to maintain growth, or at least the status quo, the ripple effect created by lack of sales has been noticeable. The Labor Department reports increases in those filing for unemployment at six times the rate of analysts’ expectations.

New construction is not the only area that has fizzled. The National Association of Realtors reported that sales of existing homes from April to June 2007 declined in 41 of 50 states and one-third of the country’s major metropolitan areas experienced price declines in the housing market (Associated Press).

Although there are numerous factors contributing to the housing slump, consistent low interest rates for almost a decade have played a significant role in the current crisis. Since the late 1990s, rates have stayed at unprecedented lows, pushing the housing market and lending industry to dizzying new heights.

This allowed millions of homeowners to upgrade into “dream homes” at the edge of their financial capabilities. Although this trend created a windfall in the lending industry, it also caused tremendous competition among banks as they maneuvered for new customers and encouraged homeowners to live on credit—regardless of whether they needed bigger, more expensive homes. Buyers were routinely approved for high-risk loans, second and sometimes even third and fourth mortgages in the secondary market, largely due to the overwhelming success of the industry as a whole. Encouraged by the housing and lending industries, Americans have built and bought new houses and drained their home equity at unprecedented levels.

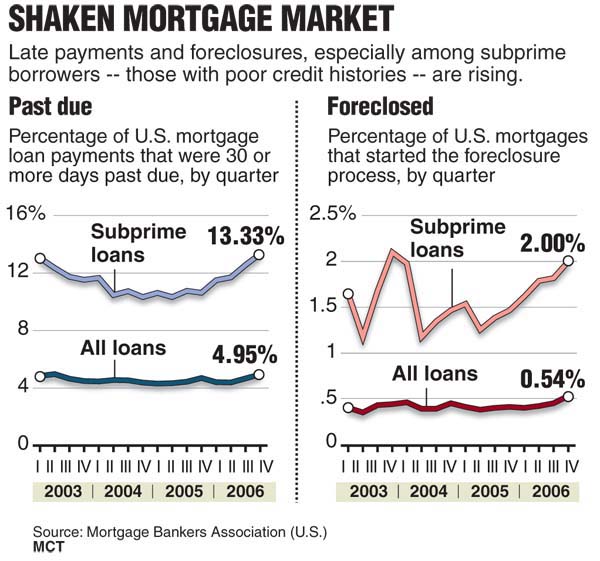

The result? Loan delinquencies and mortgage defaults have reached all-time highs in recent months.

A perfect example of the degree of this mounting crisis is the present situation for Arizona’s largest bank, JPMorgan Chase. The bank’s proportion of mortgage delinquencies to all loans surged to 1.19% in the second quarter from a minuscule 0.08% one year earlier—a delinquency rate of 15 times that of the same period just 12 months ago (The Arizona Republic).

This troubling development has driven scores of smaller lending institutions into bankruptcy and has resulted in industry giant Countrywide Financial, the nation’s largest mortgage lender, borrowing $11.5 billion dollars from a group of 40 banks to remain financially viable. The depths of the growing crisis have led to Wall Street investors and International bankers keeping an increasingly watchful eye on the troubled housing and lending industries.

National Australia Bank CEO John Stewart reported that over the next 12 to 18 months, as short term adjustable rate mortgages (ARMs) expire or reset for millions of borrowers, the $250 billion of debt given to “subprime” U.S. borrowers with bad credit profiles will be at risk. Millions of borrowers will be forced into default, extending the credit crisis even further (Business Day).

A lack of international confidence was manifested when Asian and European markets fell sharply upon the recent news.

What are the implications and what does the future hold? Opinions vary. “Looking over periods of stress that I’ve seen, this is the strongest global economy we’ve had,” said U.S. Treasury Secretary Henry Paulson in a Wall Street Journal interview.

However, a perception of a strong global economy does not necessarily translate into universal international confidence in the United States. The faltering U.S. mortgage industry and realization that many millions of Americans are living “close to the edge” financially could be the first visible cracks in a dangerously weakened economy.

More on Related Topics:

- How the Iran War and Surging Oil Prices Are Affecting Consumers at the Gas Pump and Beyond

- What to Know About the Supreme Court Ruling on Tariffs

- Credit Scores Decline for Millions as U.S. Student Loan Collections Restart

- With Retail Cyberattacks on the Rise, Customers Find Orders Blocked and Shelves Empty

- Why Are More Shoppers Struggling to Repay ‘Buy Now, Pay Later’ Loans?

Latest News

-

July 22, 2026

- Ukraine Overhauls Its Military Top Brass for the Fight Against Russia July 21, 2026

- Andy Burnham Becomes the UK’s Seventh Prime Minister in a Decade After Starmer Resigns

- Israel Is Building a Miles-Long Earthen Barrier Inside Gaza, Entrenching Its Division

- India’s Youth-led Cockroach Movement Vows to Keep Demanding Reforms After Police Crackdown

- Iran’s Forces Attack Bahrain and Kuwait After U.S. Hits Iranian Ports and Cities July 16, 2026

- Canadian Wildfire Smoke Turns Air Hazardous in the U.S. Midwest. Officials Say Stay Inside July 15, 2026

- Busy Wildfire Season Tests U.S. Fire Bosses as They Juggle Resources to Stay Ahead

- Ukraine and 9 Other Countries Announce a Coalition to Protect Europe from Ballistic Missiles July 13, 2026

- U.S. Begins New Iran Strikes After President Says Ships Will Be Charged to Use the Strait of Hormuz July 7, 2026

- Cuba Struggles to Restore Power to Island Following Nationwide Grid Collapse

- Wildfires Rage in Portugal, Greece and Spain While Greek Authorities Warn of Toxic Smoke July 1, 2026

- Analysis: Russia Pounds on the Gates of Ukraine’s ‘Fortress Belt’ June 29, 2026

- Europe’s Record Heat Has Overwhelmed Paris Mortuaries and Left Families in Distress

- The Strait of Hormuz’s Future Is Unsettled in Wake of Latest Strikes June 26, 2026

- Solving the Mystery of Melchizedek

- Global Trade in Cocaine, Methamphetamine Is Booming, UN Drug Report Shows

- The Widening Gap Between Rich and Poor Nations

- Ukraine Unleashes One of Its Heaviest Drone Bombardments of Russia

- Venezuelans Take Search for the Missing into Their Own Hands as Earthquake Death Toll Climbs

- Deadlier Than Fentanyl: Weapons-Grade Carfentanil Surges